- Weekly Wizdom

- Posts

- November 2024

November 2024

Monthly Report

United States

Once again, there is no definite direction for the US housing market. We had a reversal of the pattern from last month, with the newly built homes declining and having one of their worst declines in recent years. We saw a very strong reading last month and had impacts from the hurricanes, so this should generally be considered an outlier for now. Existing home sales seem to have bottomed for the short term, while mortgage rates are somewhat more stabilized. Finally, the house indexes have outperformed their latest monthly and yearly forecasts.

The National Association of Home Builders (NAHB)/Wells Fargo Housing Market Index increased 3 points to 46 in November, the highest level since April. The index for single-family sales moved up 2 points, and the index for prospective buyer traffic was up 3 points to 32. The largest mover was the index for sales in the next six months, which jumped 7 points to 64, the highest level since April 2022.

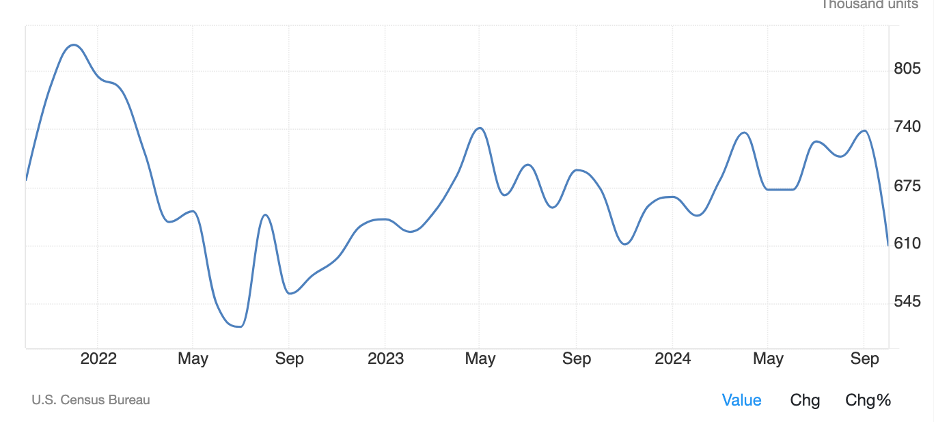

Sales of new homes in the United States plummeted by 17% in October compared to September to a seasonally adjusted rate of 610,000. This constitutes the largest drop since 2013 and a big miss from the 730,000 expected. The hurricanes impacted this, so it would be important to see how the figure changes next month. Permits remained steady, implying that this might be an anomaly due to the hurricanes.

New Home Sales - Trading Economics

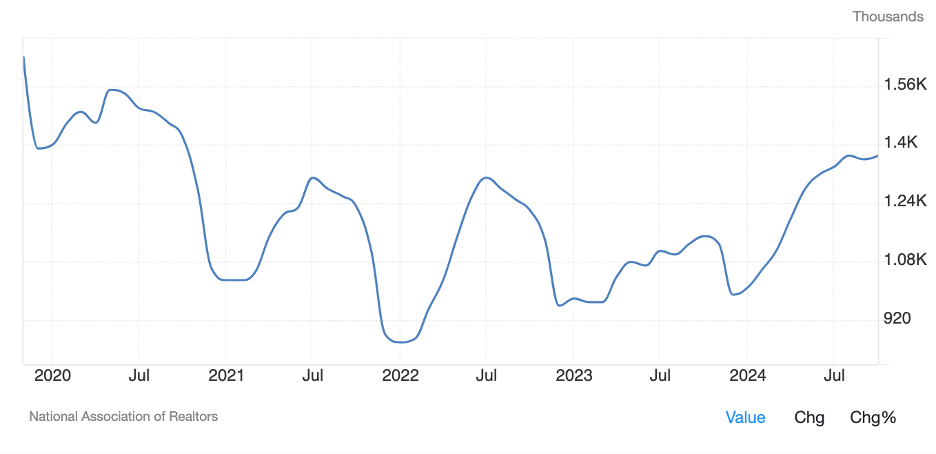

There is no new data for existing home sales. As a reminder for October, existing home sales increased 3.5% MoM to a seasonally adjusted annualized rate of 3.96 million, rebounding from the 14-year low of 3.83 million. In comparison, the number of homes on the market rose just 0.7 percent; therefore, the months’ supply fell one-tenth to 4.2. Compared to a year ago, the NAR’s measure of the median sales price of existing homes was up 4.0 percent.

Existing Home Sales - Trading Economics

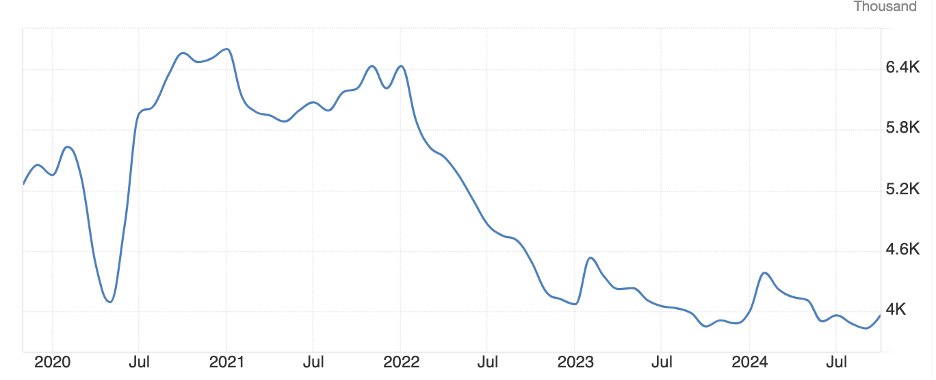

The number of homes available has risen by 1.5% to 1.4m, constituting the 10th consecutive monthly increase. Housing inventory has been at its highest level since late 2020.

US Total Housing Inventory – Trading Economics

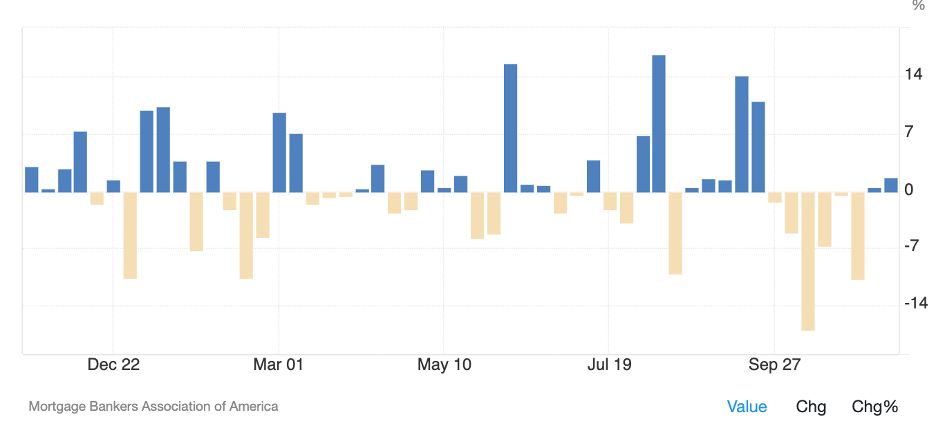

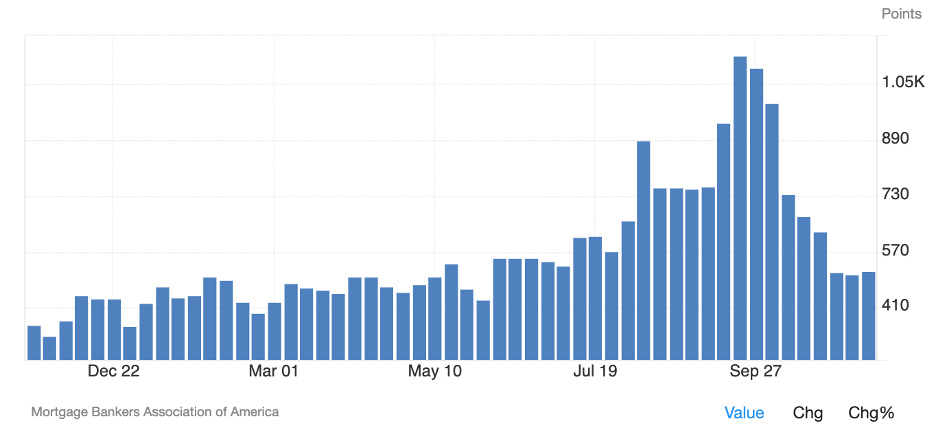

Mortgage application volumes are more than 30% lower from the end of September, reflecting the rise in mortgage rates.

Mortgage Applications - Trading Economics

The Mortgage refinancing index has been tumbling since peaking towards the end of September, with seven consecutive weeks of declines. It would be interesting to see whether it stabilizes after increasing slightly from last week.

Mortgage Refinancing Index - Trading Economics

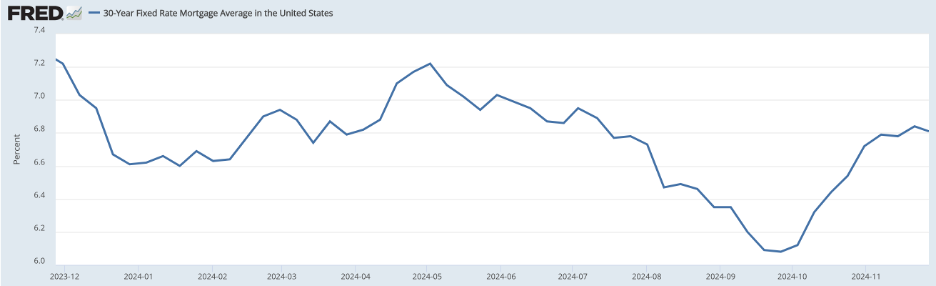

The average 30-year fixed-rate mortgage continues its uptrend, moving 10bps during November. It has now reached its highest level since July.

FRED, 2024

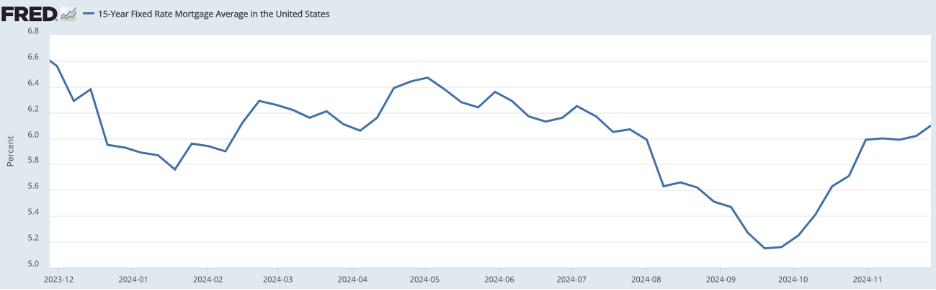

It's a very similar picture for the 15-year mortgage rate.

FRED, 2024

United Kingdom

Overall, the UK Economy is in a mixed situation. The BoE continues to cut rates, but unemployment and inflation came out higher than expected in their latest readings. Retail sales have also posted an unexpected drop this month.

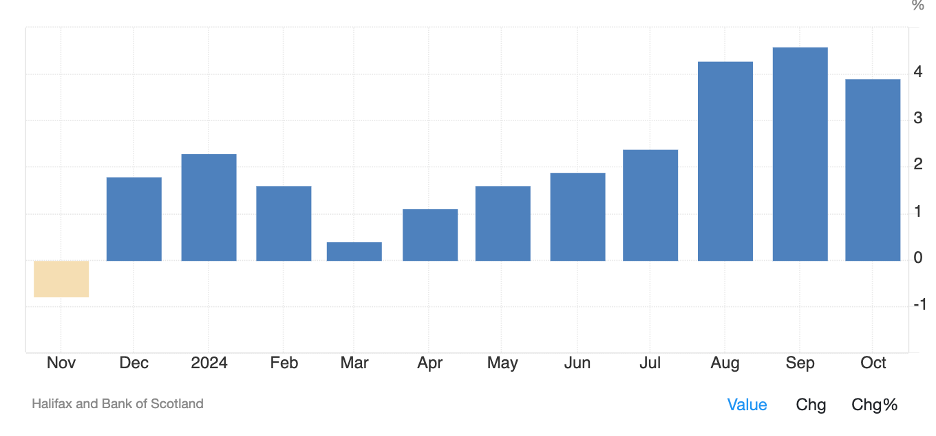

The house price Index in the UK continues to grow year on year. However, October's growth didn’t meet expectations (3.9% vs. 4.2%) and dropped from the 4.7% YoY we saw for September. Still, we have seen 11 months of consecutive YoY growths, most of which have been higher than 2%.

House Price Index YoY - Trading Economics

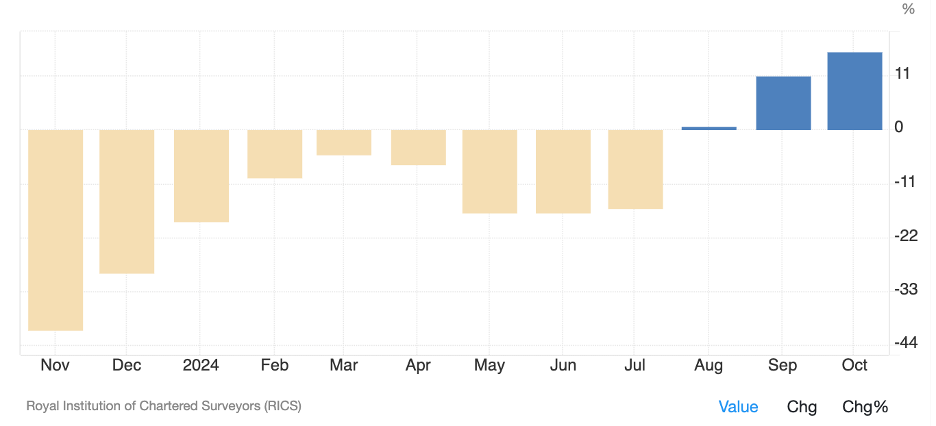

The RICS UK Residential Market Survey's house price balance tracks the difference between the percentage of respondents reporting price increases versus those predicting drops. The reading has rallied to +16% for October, up from 11% in September to 0% in August, exceeding expectations for a +11. This is also the highest level in the last two years.

Individual regions, such as London, Northern Ireland, Scotland, the Northeast, and the North West, reported positive price balances. All regions of the UK are forecasted to see house price increases over the next year, with most of the growth occurring in the North (Ireland, Scotland).

RICS House Price Balance - Trading Economics

China

China might stabilize at the macro level, as the Manufacturing index has been around 50 for two consecutive months. China's retail sales increased by 4.8% YoY in October 2024, accelerating from a 3.2% rise in the previous month and exceeding expectations for a 3.8%. It was the fastest growth in retail turnover since February, likely impacted by a week-long holiday, the recent shopping festival, and all the stimulus since September.

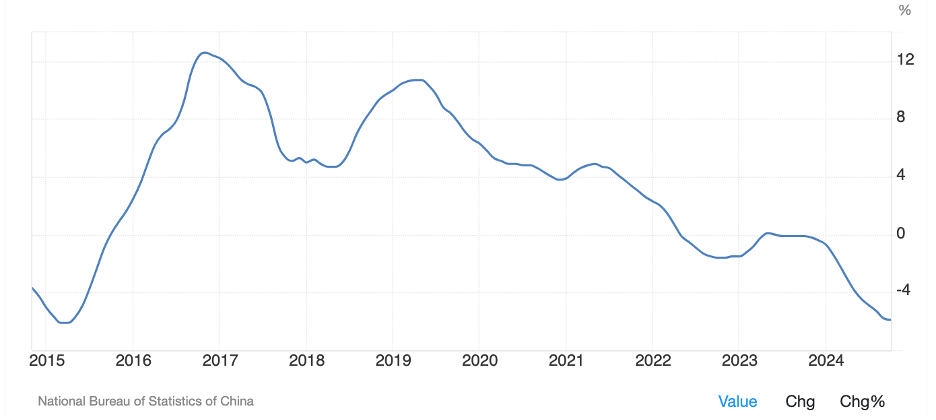

However, The property market isn’t showing any signs of recovery, with the home price index printing another strong decline. This marked the 16th consecutive month of decrease and, again, the biggest YoY drop since 2015. The latest house price index showed a 5.8% drop YoY from the 5.7% drop last month.

China Newly Built House Prices YoY Change - Trading Economics

WANT MORE?

We’ll make it easy for you! Upgrade to Premium and gain an edge in the markets with industry-leading insights and analysis.

References

(n.d.). US Treasuries Yield Curve. US Treasuries Yield Curve. https://www.ustreasuryyieldcurve.com/

(n.d.). CME FedWatch Tool. CME Group. https://www.cmegroup.com/markets/interest-rates/cme-fedwatch-tool.html

(n.d.).Trading Economics. Trading Economics. https://tradingeconomics.com/united-states/nahb-housing-market-index

(n.d.).Goldman Sachs. Goldman Sachs. https://www.goldmansachs.com/

(n.d.).Bloomberg. Bloomberg. https://www.bloomberg.com

(n.d.). FRED. Federal Reserve Economic Data. https://fred.stlouisfed.org/

Disclaimer

Wizard of Soho LLC and Weekly Wizdom publish financial information based on research and opinion. We are not investment advisors, and we do not provide personalized, individualized, or tailored investment advice, nor do we provide legal advice or information. The publisher does not guarantee the accuracy of the information provided on this page. All statements and expressions present are based on the author's or paid advertiser's opinion and research. Directly or indirectly, no opinion is an offer or solicitation to buy or sell the securities or financial instruments mentioned.

As news is ever-changing, the opinions included should not be taken as specific advice on the merits of any investment decision. Investors should pursue their investigation and review of publicly available information to make decisions regarding the prospects of any company discussed. Any projections, market outlooks, or estimates herein are forward-looking and inherently unreliable. They are based on assumptions and should not be construed to be indicative of actual events that will occur.

Contrarily, other events that were not considered may occur and significantly affect the returns or performance of the securities discussed herein. The information provided is based on matters as they exist on the date of preparation and do not consider future dates. As a result, the publisher undertakes no obligation to correct, update, or revise the material in this document or provide any additional information. The publisher, its affiliates, and clients may currently or foreseeably have long or short positions in the securities of the companies mentioned herein. They may, therefore, profit from fluctuations in the trading price of the securities. There is, however, no guarantee that such persons will maintain these positions. Unauthorized reproduction of this newsletter or its contents by photocopy, facsimile, or any other means is illegal and punishable.

Neither the publisher nor its affiliates accept any liability for any direct or consequential loss arising from any use of the information contained herein. By using the website or any affiliated social media account, you consent and agree to this disclaimer and our terms of use.